A Trust is an “agreement” between the settlor and the trustee in which the settlor transfers the legal ownership, dominion and control of the assets to trustees for the benefit of the beneficiaries pursuant to a Trust Deed.

An arrangement for the holding and administration of property under which property or legal rights are vested by the owner of the property (the Settlor) in a person or persons (the Trustees). The Trustees then hold the property for or on behalf of other persons (the Beneficiaries).

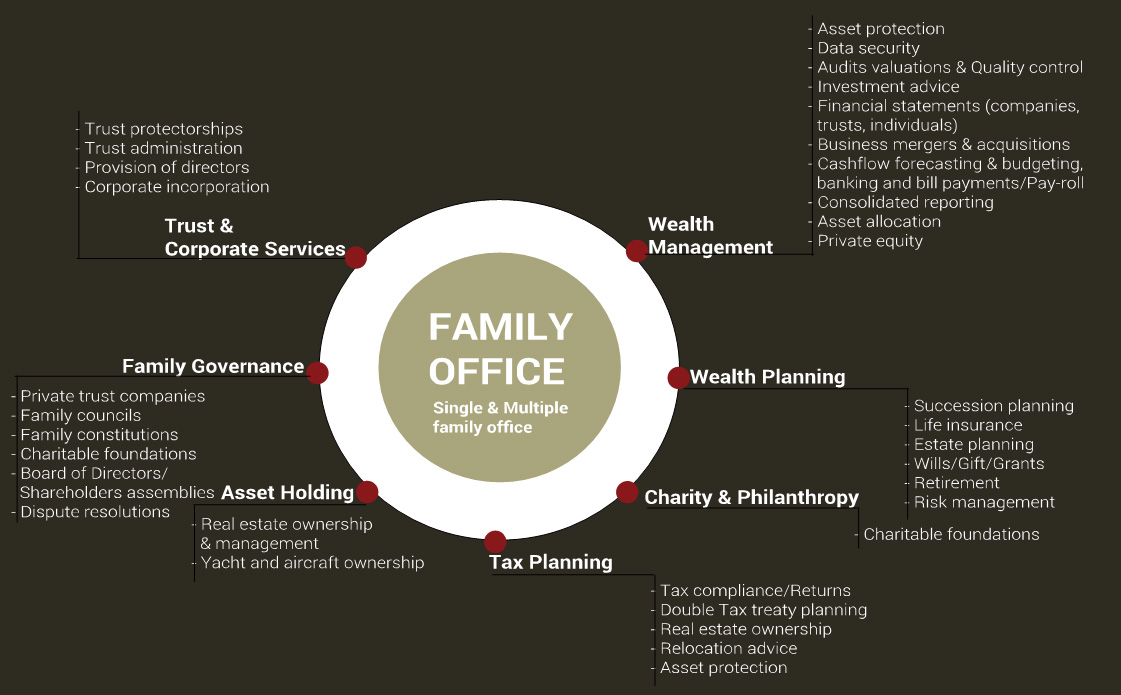

Key aspect of Trusts as does estate planning. Continuity of ownership is also secured through a holding by a Trust.

Tax Planning – A properly established Trust may produce substantial savings in income tax, capital gains tax and inheritance tax/estate duty;

- Avoiding Probate – Estate Planning – Protection against creditors

- Tax implications

Mauritius Trusts is now subject to an income tax at the rate of 15% on its chargeable income. However, a trust which is non-resident will still be exempted from taxation.

A Trust is deemed to be non-resident if its central management and control is outside Mauritius that is;

1. the trust is administered in Mauritius and a majority of the trustees are not resident in Mauritius;

2. the settlor of the Trust was not resident in Mauritius at the time the instrument creating the trust was executed or at such time as the settlor adds new property to the trust; and

3. a majority of the beneficiaries or the class of beneficiaries appointed under the terms of the trust are not resident in Mauritius

- A non-resident trust shall be liable to taxes only if it has chargeable income attributed to Mauritian source income.

- A non-resident trust shall however be required to submit a return of income to the Mauritius Revenue Authority (MRA). The return of income shall specify all income derived by it during the preceding income year and such other particulars as may be required by the MRA.

South African (“SA”) tax perspective, is the place of effective management (“PoEM”) of that trust. South Africa charges tax on a residency basis, and for a juristic person such as a trust, it would qualify as a SA tax resident where it has its PoEM in South Africa. Whilst the effective management of an offshore trust should always be considered based on its own facts and circumstances, it is pertinent to ensure that the SA settlor does not control the actions and affairs of the offshore trust to the exclusion of the offshore trustees. The offshore trustees must be able to evidence that management and control of the trust occurs in Mauritius.